Key Takeaways

It's important to know what D&O insurance includes to understand when and how it is used. This article will discuss what D&O insurance does, why it's good, and what influences it.

It's important to know what D&O insurance includes to understand when and how it is used. This article will discuss what D&O insurance does, why it's good, and what influences it.

Directors and Officers (D&O) insurance is very important for protecting the personal belongings of company leaders. This insurance helps top bosses by covering them if something goes wrong while doing their jobs.

D&O insurance helps pay for any legal costs, settlements, and other expenses if these leaders are sued for making mistakes in their roles. This means if they are taken to court, the insurance helps cover the money needed for their defense.

It's important to know what D&O insurance includes to understand when and how it is used. This article will discuss what D&O insurance does, why it's good, and what influences it.

Directors and Officers (D&O) insurance provides essential protection for corporate leaders against a variety of risks.

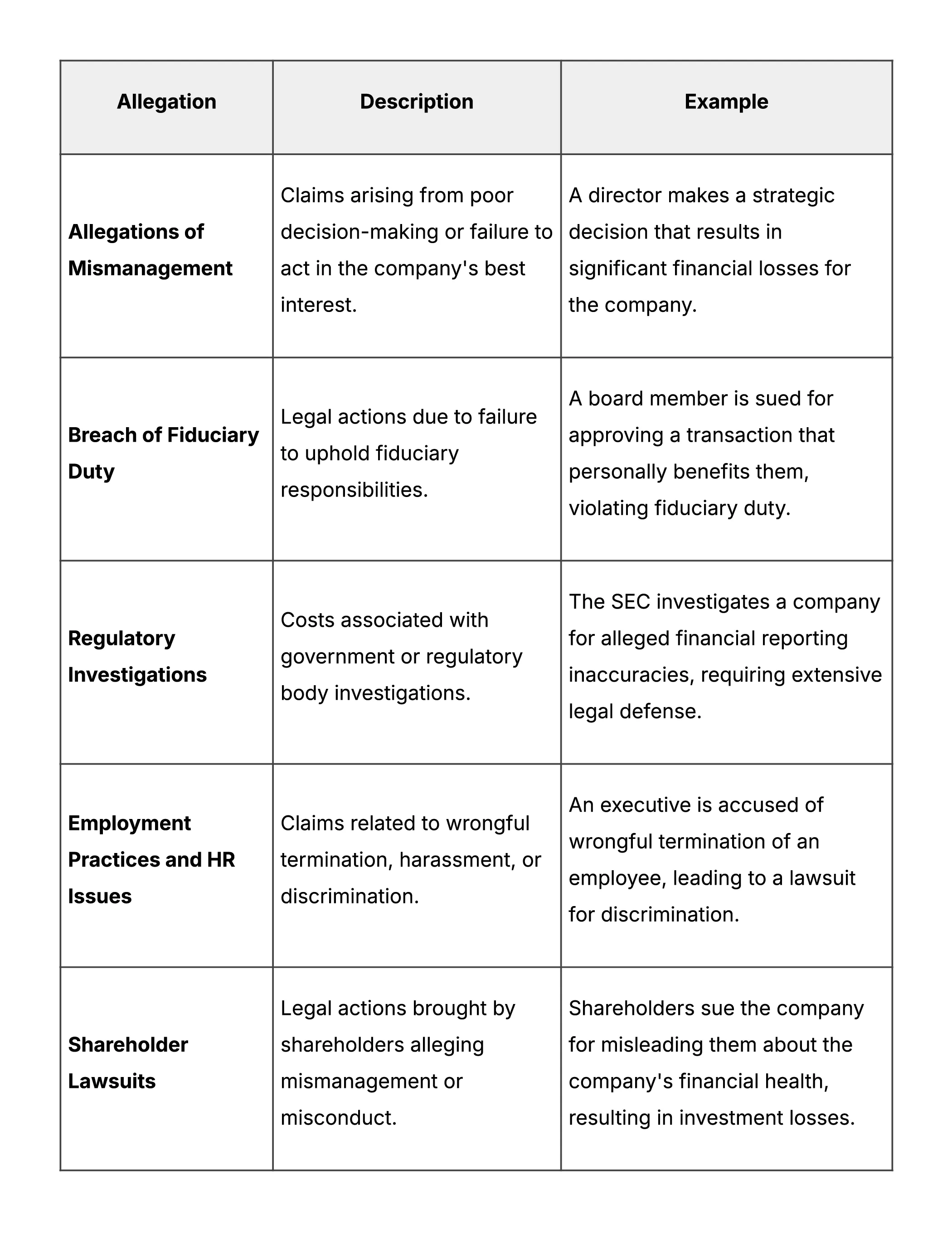

For instance, if a company faces a lawsuit due to alleged mismanagement during a merger, the directors may be personally liable for any resulting financial losses. In this scenario, D&O insurance would cover the legal defense costs and any settlements, protecting the directors' personal assets.

Below is a detailed overview of the key features and coverage areas of D&O insurance:

By understanding these comprehensive coverage areas, directors and officers can better appreciate the full scope of protection offered by D&O insurance, ensuring that they are adequately safeguarded against a wide range of potential risks.

D&O insurance is designed to protect those in high-level management and decision-making roles within an organization. Below is a breakdown of the typical policyholders who benefit from D&O insurance

Directors and Officers: High-level management positions including CEOs, CFOs, COOs, and board members responsible for strategic decision-making and overall governance.

Senior Executives: Key decision-makers such as vice presidents, general managers, and other senior leadership roles who influence significant corporate policies and operations.

D&O insurance is relevant across various industries, each with unique needs and risks. Whether a company is publicly traded, privately held, a non-profit organization, or a start-up, the leadership faces potential liabilities.

This section explores how D&O insurance applies to different types of organizations, highlighting the specific risks they encounter.

.webp)

Directors and officers can face a variety of legal challenges and claims in their professional roles. This section outlines common scenarios where D&O insurance proves vital. From allegations of mismanagement to regulatory investigations, understanding these situations helps illustrate the importance of having D&O coverage in place.

D&O insurance offers numerous advantages that extend beyond merely protecting personal assets. This section delves into the key benefits, such as attracting and retaining talent, mitigating financial risks, and enhancing corporate governance. Understanding these benefits can help organizations appreciate the broader impact of D&O insurance.

While D&O insurance provides extensive protection, it's important to be aware of its exclusions and limitations. This section covers common exclusions in D&O policies and highlights claims that may not be covered. Knowing these limitations is crucial for ensuring that directors and officers are fully aware of their coverage.

Various factors can influence the cost of D&O insurance premiums. Understanding these factors helps organizations better prepare and budget for this essential coverage. Let’s take a look at how company size, industry risk profile, claims history, and corporate governance practices affect D&O insurance premiums.

Implementing D&O insurance effectively requires careful planning and ongoing management. This section outlines best practices, including assessing the need for coverage, choosing the right policy, conducting regular policy reviews, and integrating D&O insurance with overall risk management strategies.

D&O insurance is a critical tool for protecting the personal assets of company leaders and ensuring the smooth functioning of the organization. It mitigates financial risks and enhances corporate governance, making it indispensable in today’s litigious environment.

By investing in robust D&O coverage, organizations can ensure that their top management is well-protected and can lead with confidence and integrity. Invest in Pazcare’s D&O insurance to protect against unforeseen risks. Keep your leaders confident and secure.

Directors and Officers liability insurance provide coverage to directors, officers, and other high-ranking employees against personal liability or claims due to any wrongful act or decisions. This includes Legal representation costs, Public Relations expenses and many more to which the coverage can be extended.

D&O insurance provides coverage for directors and officers of a company against claims alleging wrongful acts, such as negligence or breach of duty, which can result in legal fees, settlements, and judgments.

Here are the most common exclusions under the Director & officers liability insurance -

In India, the Director & officers liability insurance commonly known as D&O insurance is not mandatory. However, as a prudent risk management approach every company can purchase the D&O insurance policy.

Best pricing for you.

Best claim support for your team.

AICPA SOC 2

.svg)

ISO 27001

.svg)

ISNP

App for employees