Key Takeaways

In business insurance, it's super important to understand two main types: Directors & Officers (D&O) and Errors & Omissions (E&O) insurance. This article will explain how these two types of insurance are similar and different.

In business insurance, it's super important to understand two main types: Directors & Officers (D&O) and Errors & Omissions (E&O) insurance. This article will explain how these two types of insurance are similar and different.

Understanding the different types of insurance coverage is crucial for protecting businesses from various risks. In the realm of corporate insurance, distinguishing between Directors & Officers (D&O) and Errors & Omissions (E&O) insurance is particularly important.

This article will help you understand the differences and similarities between D&O insurance vs E&O insurance.

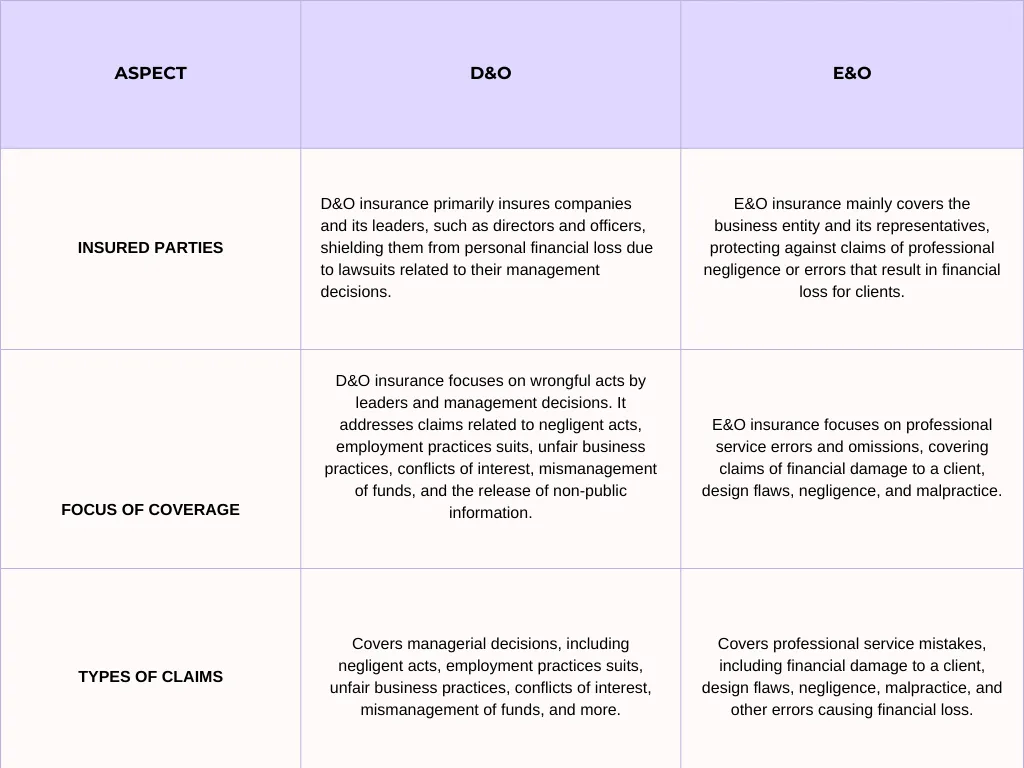

D&O insurance provides essential protection to a company and its directors and officers against financial losses if they are sued for alleged wrongful acts committed while managing the company. These acts can include negligence, breach of duty, or misrepresentation.

D&O insurance applies to company leaders, such as directors and officers, shielding them from personal financial loss due to lawsuits related to alleged wrongful management decisions.

This type of insurance is essential for any organization where management decisions can lead to significant legal actions.

D&O insurance covers a variety of claims, including:

Ensure your leadership has the peace of mind to make strategic decisions. Get a D&O insurance quote from Pazcare.

E&O insurance, on the other hand, protects businesses against allegations of failure to provide professional services or causing financial damage to clients. It covers both the representatives of the business and the business entity itself.

E&O insurance is designed to protect businesses and their employees from claims of professional negligence or errors that result in financial loss for clients. This coverage is vital for service providers who can be sued for professional erroneous mistakes or oversights.

E&O insurance typically covers claims such as:

Despite their differences, D&O and E&O insurance share some significant similarities:

1. Claims Basis: Both D&O and E&O insurance policies are written on a claims-made basis. This means they provide coverage for claims made during the policy period, regardless of when the alleged incident occurred. This aspect is crucial for ensuring that the policy responds to current claims even if the events happened in the past.

2. Allegations Coverage: Both types of insurance respond to claims alleging a wrongful act. In D&O insurance, this includes wrongful acts related to management decisions, such as breach of fiduciary duty or mismanagement of funds.

In E&O insurance, it covers professional errors or omissions, such as negligence or malpractice. Both policies provide legal defense and coverage for damages, ensuring that the insured parties are protected against financial loss arising from these claims.

3. Legal Defense: Both D&O and E&O insurance policies typically include provisions for covering legal defense costs. This is crucial as legal fees can be substantial, and having insurance coverage can significantly alleviate the financial burden on the insured party during litigation.

4. Protection Against Financial Loss: Both types of insurance aim to protect the insured from significant financial loss. Whether it's a director facing a lawsuit for a management decision or a professional being sued for a service error, these policies provide financial support to cover settlements, judgments, and associated legal costs.

Understanding the key differences between D&O insurance vs E&O insurance is essential for selecting the right coverage. Here's a detailed comparison to help you make an informed decision:

Also read: Difference between group insurance and ESI

Here are some common scenarios where D&O insurance is essential:

E&O insurance protects against different types of professional errors:

Determining whether a business needs both D&O and E&O insurance depends on various factors, including the business structure and industry.

For many businesses, both types of insurance are essential. D&O insurance is crucial for protecting the personal assets of directors and officers from risks associated with managerial decisions.

In contrast, E&O insurance is vital for protecting against lawsuits stemming from professional service errors or negligence. Understanding the unique risks a business faces can help in deciding the appropriate coverage.

It is important to consult with an insurance professional to assess your risks and tailor coverage to your specific needs.

Are you looking for comprehensive health coverage for your employees? Choose Pazcare Corporate Health Insurance and invest in their well-being.

Understanding the differences between D&O and E&O insurance is vital for comprehensive business protection. Both types of insurance play unique roles in safeguarding your business from different risks. Consulting with a professional can help determine the appropriate coverage for your organization, ensuring that both management decisions and professional services are adequately protected.

By understanding D&O insurance vs E&O insurance, informed decisions can be made to protect a business effectively. Whether you're considering D&O E&O insurance or wondering what the difference is between D&O and E&O insurance, knowing the specifics can help in choosing the right policies.

Best pricing for you.

Best claim support for your team.

AICPA SOC 2

.svg)

ISO 27001

.svg)

ISNP

App for employees