Surprised by your medical bills? Know the exclusions in your insurance policy

Exclusions in insurance, common exclusions in health insurance, permanent exclusions in health insurance, types of exclusions in insurance

Pazcare team

Team Pazcare

This is some text inside of a div block.

Updated on:

August 14, 2025

Share

Table of Contents

Key Takeaways

Health insurance plans, including group health insurance, don’t cover every medical expense, these uncovered treatments or conditions are called exclusions. Common exclusions include cosmetic surgeries, dental procedures, infertility care, and alternative therapies. Employers and individuals can also use OPD wallets and wellness packages to fill these gaps, ensuring more comprehensive healthcare coverage and fewer surprises at claim time.

Health insurance plans, including group health insurance, don’t cover every medical expense, these uncovered treatments or conditions are called exclusions. Common exclusions include cosmetic surgeries, dental procedures, infertility care, and alternative therapies. Employers and individuals can also use OPD wallets and wellness packages to fill these gaps, ensuring more comprehensive healthcare coverage and fewer surprises at claim time.

Let us imagine Tarun and Shivani are working in the same organization. Tarun is hospitalized for a covid infection and Shivani decides to get a cosmetic procedure done. Tarun spends close to Rs.50,000 on his medical bills whereas, Shivani spends around Rs.75,000 on the procedure. After discharge, they decide to raise a health insurance claim as they have an active group health insurance policy.

For Tarun, the TPA approves the claim and he gets the money spent on the medical bills reimbursed. On the other hand, Shivani’s claim gets rejected. The health insurance TPA informs Shivani that cosmetic procedures are not covered in her insurance plan. Cosmetic procedures are mentioned as exclusions in the insurance policy hence, the claim is rejected.

Now, why did this happen?

Shivani was unaware of the exclusions mentioned in her GHI policy. As a result of which she had to pay it on her own.

This example shows why it’s essential to read and understand your insurance policy’s exclusions before getting any treatment.

Exclusions in health insurance, what is it?

Always know that your health insurance plan will not cover every medical expense of yours and there are certain exclusions in the insurance policy. A health insurance plan, individual or group plan generally covers most diseases and treatments. However, there are certain treatments and medical conditions which are not covered by your plan. These are known as exclusions in a health insurance policy.

These are always clearly mentioned in your insurance contracts. So just like Shivani, you will have to pay the medical bills out of your pockets when you raise a claim for such exclusions.

However, in an individual health insurance plan, pre-existing diseases are covered after a certain waiting period. Hence, they are considered exclusions during the waiting period.

However, your group plan is different. It covers your pre-existing diseases from day 1 with 0 waiting period.

So, as long your group plan is considered, pre-existing diseases and waiting periods are not exclusions in your health insurance plan.

Both individual and group health insurance plans cover most illnesses and treatments, they have specific exceptions.

15 Common exclusions in your insurance policy

Understanding what your group insurance policy does not cover is just as important as knowing what it does. Here's a breakdown, highlighting key exclusions that HR leaders and employees should be aware of:

Permanent exclusions in health insurance

Permanent exclusions in health insurance policies are those treatments and conditions which will be never covered in your plan at any point in time. They are permanently excluded from your health insurance. These include HIV, Alzheimer’s, AIDS, congenital diseases, damages due to war or nuclear weapons, etc.

Cosmetic treatments

Cosmetic treatments or surgeries which enhance the appearance of people are generally not covered in your group insurance policy. However, plastic surgeries or reconstructive treatments due to accidents, burns or cancer may be covered in your policy depending on its terms and conditions.

Injuries due to self-harm

Treatment expenses generated due to injuries caused by suicide attempts or any other self-harm are not included in your policy.

Substance abuse/alcoholism treatments

Expenses related to treatments or procedures on the account of substance abuse, alcoholism or any other addiction are excluded from coverage.

Alternative treatments

Your group health insurance policy does not cover expenses generated due to alternative treatments like naturopathy, acupuncture, magnetic therapies or any such treatments.

Other exclusions in the health insurance policy

According to the IRDAI circular, there is a standard list of exclusions for your health insurance contracts. However, a few like pre-existing diseases and waiting periods do not apply to a group insurance policy.

Hence, other exclusions in your group policy will be

Dental treatment

Dental treatments are considered cosmetic procedures by the insurer. Hence, expenses due to dental treatments are not covered in your policy. But dental treatments due to accidents or injury may be covered by your insurer. However, while purchasing your group plan you can add a rider plan to cover dental treatments.

Pregnancy-related treatments

Just like dental insurance, pregnancy-related hospitalization like abortion, miscarriage and other expenses towards it are not covered by default in your group policy.

Gender changing treatments

Expenses due to treatment or surgeries to change the gender of an individual are considered exclusions in your policy.

Infertility treatments

Procedures like in-vitro fertilisation (IVF), fertility medications, and related reproductive treatments are usually excluded.These are often considered elective rather than medically necessary.

Obesity Treatments

Costs related to obesity management and bariatric surgeries (e.g., sleeve gastrectomy, gastric bypass) are typically excluded. Exceptions apply only if the surgery is deemed medically necessary due to life-threatening conditions like severe diabetes or heart disease.

Dietary & health supplements

Expenses for vitamins, minerals, protein powders, or other dietary supplements are not payable unless they are part of a prescribed inpatient treatment. Over the counter purchases from pharmacies or online stores are never covered.

Hospital expenses limit

Most group health insurance policies provide you with room rent and ICU room expenses, doctor’s consultation expenses, and diagnostic tests expenses. However, there is a limit on these expenses for most plans, unless you go for an add-on cover. Read your policy wording carefully to know the conditions attached to them.

Mental illness treatment

Your group health insurance policy may not cover expenses that arise due to mental illness or disorders treatment.

Hospitalization without doctors’ recommendations

Any hospitalization expense without a doctors’ recommendation will not be covered in your group insurance plan unless it's an emergency hospitalization.

Miscellaneous expenses

Miscellaneous expenses include the cost of hearing aids, spectacles, health supplements or any other items included in the IRDAI’s list of expenses excluded category will not be covered by your insurer.

Why do health insurance plans have exclusions?

Health insurance plans have exclusions mainly to manage risk and keep premiums affordable. Here’s why insurers include them:

Prevent Misuse of Coverage – Without exclusions, people could buy insurance only after they already know they need expensive treatments.

Control Premium Costs – Covering every possible treatment, including elective or cosmetic ones, would make premiums much higher for everyone.

Focus on Medically Necessary Care – Insurers prioritise treatments that are essential for survival and recovery, not elective or lifestyle-related.

Avoid Uninsurable Risks – Some conditions, like HIV or congenital diseases, have very high, long-term treatment costs, making them financially unsustainable to insure.

Regulatory Guidelines – The IRDAI provides a standard list of permanent exclusions that all insurers must follow.

HR & employee takeaways

Read carefully: Exclusions can significantly impact your out-of-pocket costs especially for elective or niche treatments.

Clarify before treatment: Confirm with HR or TPA whether a treatment is covered to avoid surprises.

Consider add-ons: By combining Group Health Insurance with OPD wallet benefits and corporate wellness packages, employers can create a holistic health benefits ecosystem that covers gaps left by standard insurance exclusions.

Educate employees: Sharing a simplified FAQ or summary of exclusions can give transparency and trust.

How is your group health insurance experience better with Pazcare?

At Pazcare we are open with our policies. With that, we mean as an HR or an employee, you get to know what is covered and not covered in your group health insurance plan.

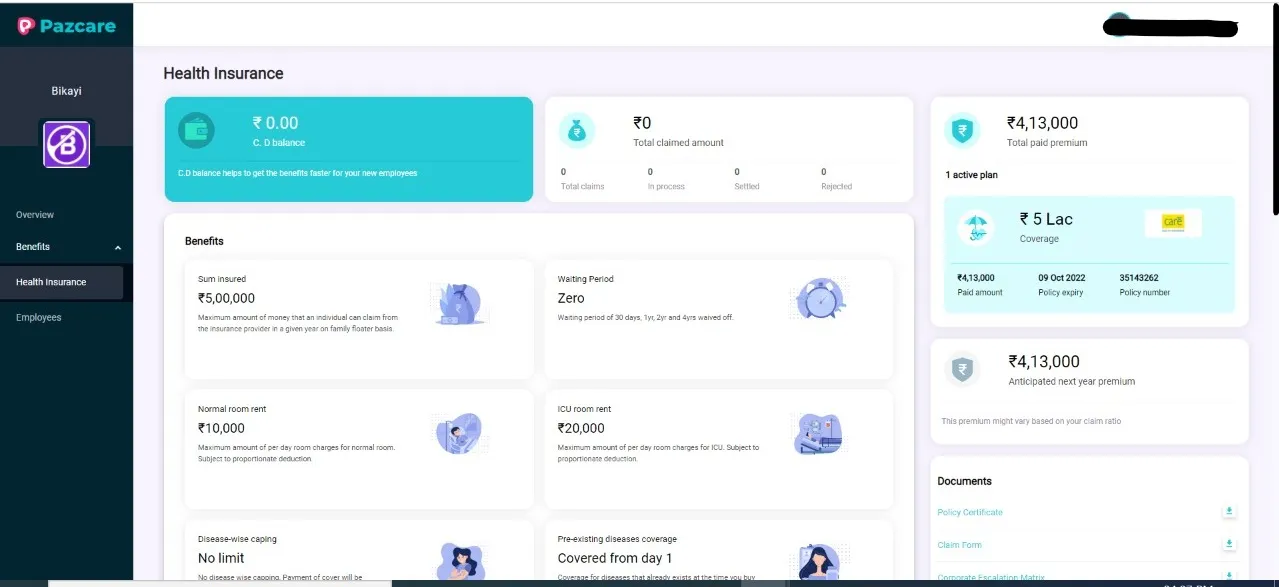

If you are an HR/ admin, access the inclusions and exclusions in your admin dashboard.

Log in →access benefits→health insurance

Admin Dashboard

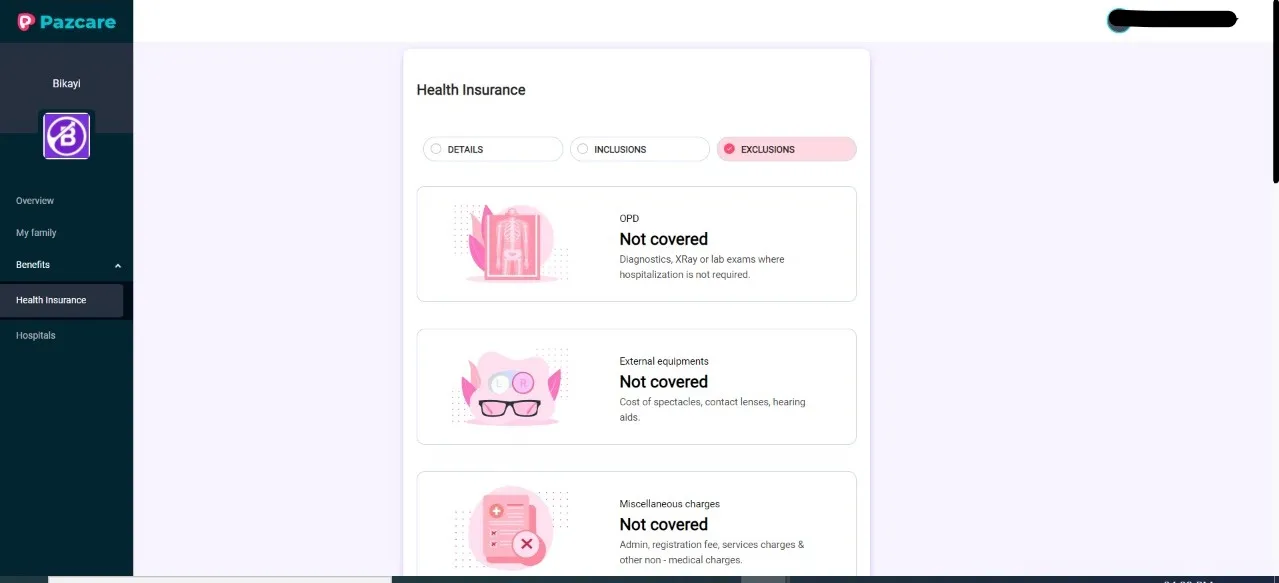

Employees can access the inclusions and exclusions in the employee dashboard.

Log in →access benefits→health insurance

Employee Dashboard

Conclusion

Purchase your group health insurance policy after you read the terms and conditions of the policy. Every health insurer has its own set of inclusions and exclusions mentioned in its policy. However, the above-mentioned ones are common exclusions in any plan. Sometimes, you can pay a higher premium and get make some like materinity, OPD and dental exclusions as inclusions. This has to be done when your buy the policy as there won't be any changes to the policy after your buy it. If you have any doubts regarding the purchase of group insurance plans for your team, contact Pazcare’s customer support, and we are more than happy to help you out.

Hereafter, don’t be surprised by your medical bills, be aware of your insurance policy.

Key takeaways

Blog sources

About the Author

Follow on:

Thanks for subscribing! If it’s your first time, check your inbox. Otherwise, you’re already on our list

Oops! Something went wrong while submitting the form.

Ready to give yourself and your team the best employee benefit experience?

Common exclusions include cosmetic treatments, infertility care, dental procedures, obesity surgeries, alternative therapies, and treatment for self-inflicted injuries.

What are exclusions in an insurance policy?

Exclusions are specific medical conditions, treatments, or expenses that your health insurance policy does not cover. These are clearly listed in the policy document.

How are the exclusions in group policies different from individual policies?

Group health insurance often has fewer exclusions compared to individual plans. For example, most group policies have zero waiting periods for pre-existing diseases and may cover maternity benefits, while individual plans usually have longer waiting periods and stricter exclusions.

What is not covered in group health insurance?

Often plastic surgeries, botox treatment, and suicide attempts are excluded from your group health insurance.

Is the family covered under group health insurance?

Yes, you can choose to add your family members to your group health insurance policy.

.svg)

.svg)