Respiratory conditions account for 4.22% of hospitalizations in Indian employee health insurance portfolios, and the real burden lives outside claims data: in absenteeism, dependent caregiving, and productivity loss that never appears on any insurance report.

Children drive 36.3% of respiratory hospitalizations and parents another 25.1%, making respiratory illness a family-driven healthcare issue, not just an employee health issue. HR teams that design coverage around the employee alone are addressing less than a third of the problem.

HR leaders can reduce respiratory claims through fast outpatient and teleconsultation access, spirometry screening for chronic disease, flu and pneumococcal vaccination, indoor air quality investment, and seasonal planning, not by tightening policy terms or denying coverage.

Respiratory conditions account for 4.22% of hospitalizations in Indian employee health insurance portfolios, and the real burden lives outside claims data: in absenteeism, dependent caregiving, and productivity loss that never appears on any insurance report.

Children drive 36.3% of respiratory hospitalizations and parents another 25.1%, making respiratory illness a family-driven healthcare issue, not just an employee health issue. HR teams that design coverage around the employee alone are addressing less than a third of the problem.

HR leaders can reduce respiratory claims through fast outpatient and teleconsultation access, spirometry screening for chronic disease, flu and pneumococcal vaccination, indoor air quality investment, and seasonal planning, not by tightening policy terms or denying coverage.

If you are an HR leader looking at your group health insurance dashboard and seeing respiratory conditions at 4.22% of hospitalizations, you are looking at the smallest, least useful part of a much bigger problem.

Coughs, colds, breathlessness, and fevers are the most visible health problems in any Indian workplace. Almost every employee deals with a respiratory illness during the year. Yet very few of them are ever hospitalized for it. That gap, between how common respiratory illness is and how rarely it shows up in claims, is the single most misread signal in employee health insurance today.

Most HR teams read this gap backward. They look at low respiratory hospitalization, conclude that respiratory illness is a minor concern for their workforce, and design coverage accordingly. This is a mistake. Low hospitalization does not mean low impact. It means most of the burden is invisible: managed quietly through outpatient care, sick leaves, dependent caregiving, and lost productivity that never appears on any insurance report.

This blog is for HR leaders who want to stop optimizing their employee health insurance policy for the wrong metric. We will look at what respiratory claims data actually reveals (and hides), why claims are rising, who is driving them, and what HR leaders can practically do to reduce both hospitalizations and absenteeism.

The gap between respiratory illness and claims data

In any group health insurance dataset, respiratory hospitalizations represent only the most severe outcomes. Most respiratory cases never escalate to a hospital bill. They are treated at home with rest, paracetamol, or a short course of medication. Only the cases that escalate, such as pneumonia, severe asthma flare-ups, and complications from delayed treatment, ever become claims.

This makes respiratory hospitalization a poor measure of workforce health. It is a much better measure of how many employees and dependents fell through the gaps in outpatient care. Here is what the data shows across Indian employee group health insurance portfolios:

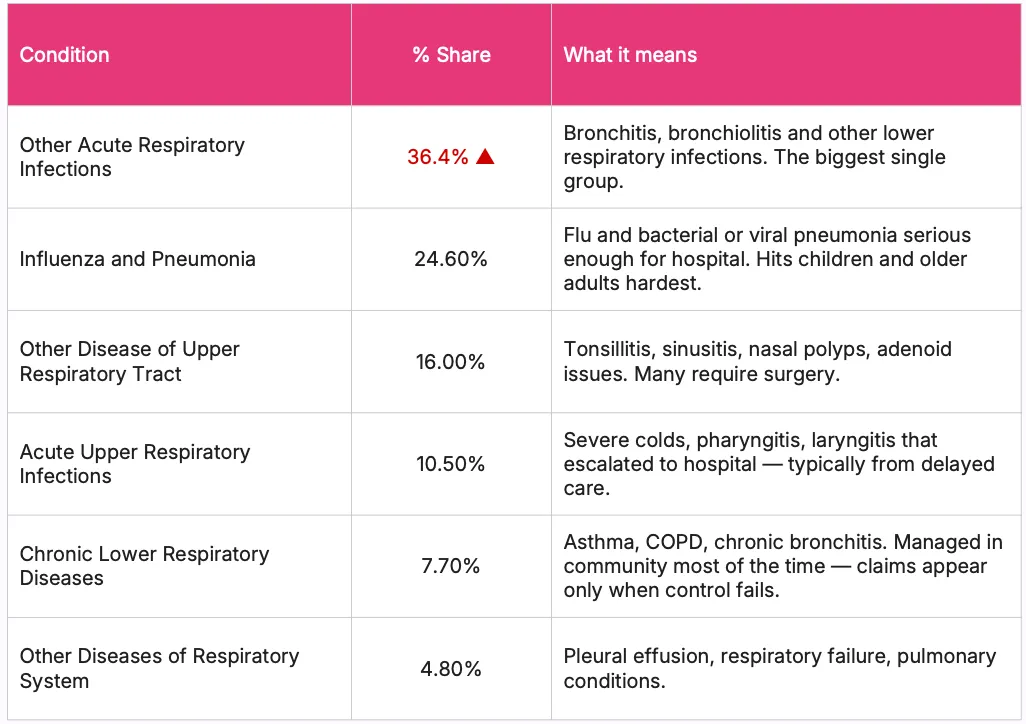

Respiratory conditions account for 4.22% of all hospitalizations.

Acute infections (bronchitis, pneumonia, upper respiratory infections) make up 71.5% of those claims.

Chronic respiratory diseases like asthma and COPD account for just 7.7% of claims, despite India having one of the highest chronic respiratory disease burdens in the world.

According to the India State-Level Disease Burden Initiative, a Global Burden of Disease study funded by the Indian Council of Medical Research and the Ministry of Health and Family Welfare, Government of India, India had 55.3 million COPD cases and 37.9 million asthma cases in 2016 alone.

According to the same study, India accounts for just 18% of the global population but 32% of the global disability-adjusted life years (DALYs) from chronic respiratory diseases.

Key insight for HR:Claims data shows the tip of the iceberg. The bigger problem, frequent illness, productivity loss, dependent caregiving, sits underneath, invisible to your spreadsheet. If you are benchmarking your respiratory burden by hospitalization volume alone, you are missing 90% of the picture.

Why respiratory claims are rising in employee health insurance

Respiratory claims are climbing across nearly every Indian organization. This is not a random trend. Several structural factors are converging at the same time, and HR leaders need to understand each one to design coverage that actually works.

1. Air pollution, not smoking, is the dominant risk factor

This is the single most important shift in respiratory health, and most HR teams have not caught up to it. According to the World Health Organization Air Quality Guidelines (2021), the safe annual mean exposure to PM2.5 is 5 µg/m³. According to the Indian National Ambient Air Quality Standards set by the Government of India, the Indian limit is 40 µg/m³, eight times the WHO recommendation. According to a 2024 Lancet Planetary Health study using India's Civil Registration System data, the entire Indian population (1.4 billion people) lives in areas where PM2.5 exceeds the WHO guideline, and 1.1 billion people (81.9%) live in areas exceeding even the more permissive Indian standard.

According to the India State-Level Disease Burden Initiative (Indian Council of Medical Research and Ministry of Health and Family Welfare), 53.7% of India's COPD disease burden is attributable to air pollution, compared to 25.4% from tobacco use and 16.5% from occupational risks. In other words, air pollution causes more of India's COPD burden than smoking and occupational exposure combined.

The Hindu reported a study by AIIMS Delhi published in 2024, 1 in 3 Delhi residents has impaired lung function even without a history of smoking. According to Central Pollution Control Board data, school children in Delhi have approximately 30% lower lung capacity than peers in cleaner Indian cities. The implication for HR is direct: your employees' lungs are being damaged on the commute and at home, long before they ever show up at a hospital.

2. Late treatment turns common illnesses into hospitalizations

A respiratory hospitalization almost always reflects something that went wrong upstream: a cold that was not taken seriously, an asthma flare-up that was not caught early, an infection that was self-medicated with antibiotics until it worsened. According to the World Health Organization, asthma is "often under-diagnosed and under-treated, particularly in low- and middle-income countries." When outpatient care is hard to access or expensive, illnesses escalate. The 71.5% acute infection share in respiratory claims is, in plain terms, a measure of how broken your outpatient pathway is.

3. Family and dependent-driven claims

Children account for 36.3% of respiratory hospitalizations, the largest single group. Parents account for 25.1%. Spouses for 8.9%. The employee themselves accounts for just 29.7%. Most respiratory claims in your employee group health insurance are not the employee. They are dependents. If your employee health insurance policy and wellness initiatives are designed around the employee alone, you are addressing less than a third of the problem.

4. Metro concentration

Metro cities account for 62.5% of respiratory claims, driven by higher PM2.5, denser commutes, and shared office environments. Non-metro locations show 37.5%, still high, shaped more by limited outpatient access than air quality. This is not a problem you can solve uniformly across geographies. Your Delhi and Mumbai offices need different interventions than your Tier 2 sites.

Want to benchmark your respiratory claims against your industry?Talk to a Pazcare expert for a complete claims analysis of your group health insurance policy.

The real cost: absenteeism and productivity loss

Here is the part that should worry HR leaders most, because it does not appear anywhere in claims data. For every respiratory hospitalization in your employee group health insurance portfolio, there are dozens of unreported episodes. Employees and dependents who managed their illness at home or through outpatient care. These cases never appear in claims, but they have a direct impact on workforce productivity. A typical respiratory illness cycle in an Indian workplace looks like this:

One employee comes to work with a cold (often presenteeism, which is itself a problem).

They infect 2 to 3 colleagues over 2 to 3 days.

Each infected person takes 1 to 2 sick days or works at reduced capacity for a week.

The team's effective output drops for 2 to 3 weeks from a single introduction.

This pattern repeats across the monsoon and winter months.

According to research summarized by the National Productivity Council of India, presenteeism (working while ill) reduces output by 33% to 75% compared to normal performance. Multiply this across a respiratory season, and the cost to a business is many multiples of what shows up in insurance claims.

This is why respiratory illness punches far above its 4.22% claim share in actual workforce impact. Claims capture only the hospitalizations. The real cost lives in the days of reduced productivity, the meetings missed, the deadlines pushed, and the cascading sick leave that a single respiratory infection can trigger across a team.

Respiratory illness affects the business more through productivity than through claims. HR leaders who ignore this pay for it twice: first in absenteeism, then in claims.

This is also why employee health and wellness programs that focus only on hospitalization coverage miss the point. The illness was already costing the business long before the claim was ever filed.

Who is driving respiratory claims in your workforce?

If HR teams want to reduce respiratory claims in their employee health insurance policy, they need to know who is actually driving them. The data here is uncomfortable for any HR leader who thinks of "employee health" in employee-only terms.

Who

% of Respiratory Claims

Typical Age

What They Bring

Children

36.3% (largest)

0–20

Pneumonia, bronchitis, tonsillitis. Young immune systems cannot contain infections adults shrug off.

Employee (self)

29.7%

20–45

Acute infections, upper respiratory tract issues. Direct productivity loss.

Mix of acute infections and upper respiratory issues.

This is not just employee health. It is family-driven healthcare utilization. Any serious effort to reduce respiratory claims has to look beyond the employee and address pediatric and parental care access.

For HR leaders, this also reframes how to think about employee wellbeing. A child's pneumonia hospitalization is paid by the insurance, but the cost is borne by the employee through emergency leave, sleepless nights, and the distraction of managing a sick child while trying to work. None of this shows up in claims data. It shows up as sudden leave requests, missed deadlines, and reduced focus during monsoon season every year, predictably.

If your employee group health insurance policy does not have strong pediatric coverage, fast pediatric outpatient access, and parent caregiving support, you are quietly subsidizing absenteeism.

Acute vs. chronic conditions: what HRs often miss

Respiratory illness comes in two forms, and they behave very differently in claims data. HR leaders who miss this distinction will design the wrong interventions.

Acute infections (bronchitis, pneumonia, upper respiratory infections) make up 71.5% of respiratory claims. These are conditions every person gets multiple times in life, and most manage with rest and basic medication. When they appear as inpatient claims, it means something failed in the outpatient pathway: the patient waited too long, self-medicated incorrectly, or had an underlying condition that turned a routine infection dangerous.

Chronic respiratory diseases (asthma, COPD, chronic bronchitis) make up just 7.7% of claims. On the surface, this looks like a small problem. It is not. According to the India State-Level Disease Burden Initiative, India has the highest number of COPD cases in the world, at 55.3 million. The reason chronic disease is underrepresented in claims is that most of it is being managed outside hospitals, which is appropriate clinical practice, but it is invisible in your data.

Key insight for HR: Low claims do not mean low risk. Chronic respiratory disease is silently growing in your workforce. The employee with uncontrolled asthma may never file a claim, but they will take more sick days, perform poorly during high-pollution periods, and face a much higher risk of a severe episode during respiratory infection season. According to the Ministry of Health and Family Welfare, Government of India, COPD is the second leading cause of death in the country after heart disease. COPD develops slowly over 10 to 20 years of exposure to air pollution, chemicals, or occupational dust. By the time it surfaces as a claim, the lung damage is permanent. The window for inexpensive management has closed long before the hospitalization.

Why respiratory illness disrupts workplaces more than other conditions

Respiratory illness hits the organization from three directions at once:

The employee falls sick. They take leave, lose focus, and reduce output.

A child or parent falls sick. The employee takes caregiving leave, manages logistics, and works while exhausted.

The infection spreads. Other team members get sick, leading to compounding absenteeism.

With children at 36.3%, employees at 29.7%, and parents at 25.1%, a respiratory season does not affect just one type of enrolled member. It creates pediatric admissions requiring caregiving leave, direct employee hospitalizations, and parent hospitalizations adding financial and emotional stress, often simultaneously.

This is what makes respiratory illness one of the most disruptive claim categories in employee health insurance, despite its per-claim cost being relatively moderate. High frequency plus moderate cost plus multi-member impact equals high total impact. Most HR teams underestimate the third factor.

What HR leaders can do to reduce respiratory claims

Reducing respiratory claims in employee group health insurance is not about denying coverage or tightening policy terms. That is what badly designed insurance does. The smart approach is to strengthen the layers that sit before a hospitalization: outpatient care, prevention, and workplace wellness. Here is what actually works for an Indian workforce in 2026.

1. Prioritize fast access to outpatient care

Early treatment is the single most effective respiratory intervention. Teleconsultation, same-day GP access, and pediatric helplines allow treatment within 24 to 48 hours of symptom onset, preventing escalation to hospitalization. A strong employee health insurance policy should include high-volume teleconsultation as a standard feature, not an add-on. If your current policy treats teleconsultation as a premium feature with caps, that is the first thing to fix at renewal.

2. Strengthen pediatric care access

Children account for 36.3% of respiratory claims. Pediatric teleconsultation, clear care pathways for parent-employees, and parent awareness on early symptom recognition help ensure early treatment and reduce hospitalization risk for the largest cost driver in your portfolio. A pediatric-first approach is the highest ROI design choice an HR leader can make in respiratory coverage.

3. Add spirometry to annual health screenings

Spirometry detects asthma and COPD early, especially in employees over 30 and those exposed to pollution or smoking. According to the Government of India's National Programme for Prevention and Control of Non-Communicable Diseases (which now formally covers COPD and asthma), spirometry is the recommended diagnostic tool for chronic respiratory disease. It remains underused even in chest physician practices. This low-cost screening significantly reduces long-term respiratory risk by catching chronic disease before it becomes a claim. Build this into your employee health and wellness programs as a default annual screening for the over-30 population.

4. Improve workplace air quality

Indoor air quality directly affects respiratory health. According to the World Health Organization, air pollution is "an important risk factor for asthma, causing new cases and making existing disease worse." Air filtration, proper ventilation, and AQI monitoring reduce disease risk, particularly in high-pollution cities like Delhi, Mumbai, and Bengaluru. HEPA filters in office spaces are not a luxury for Indian workplaces in 2026. They are infrastructure.

5. Support respiratory protection during commutes

Daily pollution exposure contributes to long-term lung damage. Providing N95 masks, flexible commute options, or remote work during high-AQI periods reduces cumulative respiratory risk. This is one of the most under-used levers in workplace wellness, and it costs almost nothing. If your AQI is over 300 and you are still mandating in-office attendance, you are creating future COPD claims.

6. Encourage employees to stay home when sick

Presenteeism increases disease spread and severity. Clear sick-leave policies and work-from-home flexibility reduce transmission and prevent complications. A team where one person works through a cold ends up with five people working through colds. The math is simple, but HR cultures that informally penalize sick leave undercut every other respiratory intervention you make.

7. Prepare for predictable seasonal surges

Respiratory claims peak during the monsoon (June to September) and winter (November to February) months. Advance awareness campaigns, early care access, and operational planning around these periods reduce hospitalization risk and workforce disruption. This is not an unpredictable risk. It is a calendar event. Plan for it the same way you plan for appraisal cycles.

8. Support tobacco cessation

Tobacco use is the second largest contributor to chronic respiratory disease in India after air pollution. According to the India State-Level Disease Burden Initiative, tobacco accounts for 25.4% of COPD DALYs in India. Workplace cessation programs reduce long-term respiratory claims and improve workforce health. Pair this with EAP support for sustainable outcomes.

9. Add flu and pneumococcal vaccination to your wellness budget

According to the World Health Organization, influenza vaccination significantly reduces influenza-related absenteeism and hospitalization. Pneumococcal vaccination prevents the most common cause of severe pneumonia. Both are inexpensive, well-evidenced, and underused in Indian corporate wellness programs. Build them into your annual employee wellness calendar.

How Pazcare helps HRs reduce respiratory claims

A strong employee health insurance policy is only the foundation. Reducing respiratory claims requires a layered approach (coverage, outpatient access, preventive care, and workplace wellness) working together.

Pazcare helps HR teams design employee group health insurance policies with strong outpatient and teleconsultation coverage, run preventive screening programs that catch chronic respiratory conditions early, and deliver employee health and wellness programs built around real claims data, not assumptions.

If your respiratory claims are climbing, the answer is rarely a stricter policy. It is a smarter one.

Talk to a Pazcare expert to review your respiratory claims data and design coverage that reduces both hospitalizations and absenteeism.

Conclusion

Respiratory illness is the most common health problem in any Indian workplace and the least visible in your claims data. The 4.22% share you see in your group health insurance dashboard is the tail end of a much larger iceberg, one that lives in sick leaves, missed deadlines, dependent caregiving, and the slow erosion of productivity during pollution and infection seasons.

Here is the direct message for HR leaders: you cannot manage respiratory burden by reading hospitalization data alone. You will always be solving for the smallest, most expensive part of the problem. The HR leaders who treat respiratory health as a workforce health problem, and design coverage, screening, and wellness around early outpatient care, will see lower claims, lower absenteeism, and a healthier, more present team. The ones who treat it as a claims-only problem will keep paying for hospitalizations they could have prevented. That is what employee wellbeing actually looks like in 2026.

Talk to a Pazcare expert to review your respiratory claims data and design coverage that reduces both hospitalizations and absenteeism.

Anupika Khare, Marketing Manager at Pazcare, turns complex ideas into stories that resonate with HR leaders and business decision-makers. With expertise in media, copywriting, and SEO-led marketing, she creates content that informs, inspires, and drives conversations on workplace wellness and benefits.

Follow on:

Thanks for subscribing! If it’s your first time, check your inbox. Otherwise, you’re already on our list

Oops! Something went wrong while submitting the form.

Ready to give yourself and your team the best employee benefit experience?

Yes, COPD is generally covered under group health insurance policies as part of standard hospitalization benefits. Coverage typically includes hospitalization expenses, ICU care, and prescribed inpatient treatment. However, ongoing outpatient management (inhalers, regular consultations, pulmonary rehabilitation) may require separate OPD coverage or a wellness rider. According to the Ministry of Health and Family Welfare, Government of India, COPD is the second leading cause of death in India after heart disease, so HR leaders should review their employee health insurance policy to confirm both inpatient and outpatient COPD support.

Why are respiratory illnesses important in workplace wellness?

Respiratory illnesses are the most frequent reason for sick leave in Indian workplaces, and they spread quickly across teams. Even though they account for only 4.22% of hospitalizations, they create the highest volume of absenteeism, productivity loss, and dependent caregiving leave. A strong workplace wellness program that addresses respiratory health (through air quality, screening, vaccination, and early outpatient access) has one of the highest returns on investment of any wellness initiative an HR team can fund.

How can HR improve employee respiratory health?

HR teams can improve employee respiratory health by enabling fast outpatient and teleconsultation access, adding spirometry to annual health screenings, improving indoor air quality, providing flu and pneumococcal vaccinations, supporting protective measures during high-AQI periods, and building strong sick-leave culture so employees stay home when ill. Pediatric care access matters too, since children drive over a third of respiratory claims in employee group health insurance.

Are respiratory illnesses preventable?

Most acute respiratory illnesses are preventable or controllable through early outpatient care, vaccination (flu and pneumococcal), good indoor air quality, and basic infection-prevention practices. Chronic respiratory diseases like COPD and asthma cannot be cured but can be managed effectively with early diagnosis and consistent treatment, preventing severe episodes and hospitalizations. According to the World Health Organization, asthma is "often under-diagnosed and under-treated," meaning early screening and access to inhaled corticosteroids can prevent a significant share of severe episodes.

Is bronchitis covered by group health insurance?

Acute bronchitis requiring hospitalization is covered under standard group health insurance policies as part of hospitalization benefits. Most cases of bronchitis, however, are managed on an outpatient basis and would fall under OPD coverage if your employee health insurance policy includes it. Severe or complicated bronchitis cases that lead to inpatient admission are covered as part of regular hospitalization benefits in most employee group health insurance plans.

.svg)

.svg)